FROM OUR BLOG

May 1, 2025

In the shadow of Wall Street's gleaming towers, a quiet revolution is reshaping the investment landscape. Active fund managers—once the rockstars of finance—increasingly find themselves unable to beat simple index funds in developed markets. Yet halfway around the world, amid India's bustling financial centers, a different story unfolds: one where skilled investment managers consistently generate excess returns. This stark geographical contrast offers critical insights for investors seeking to optimize their global portfolios.

The Brutal Math: Alpha's Global Disappearance

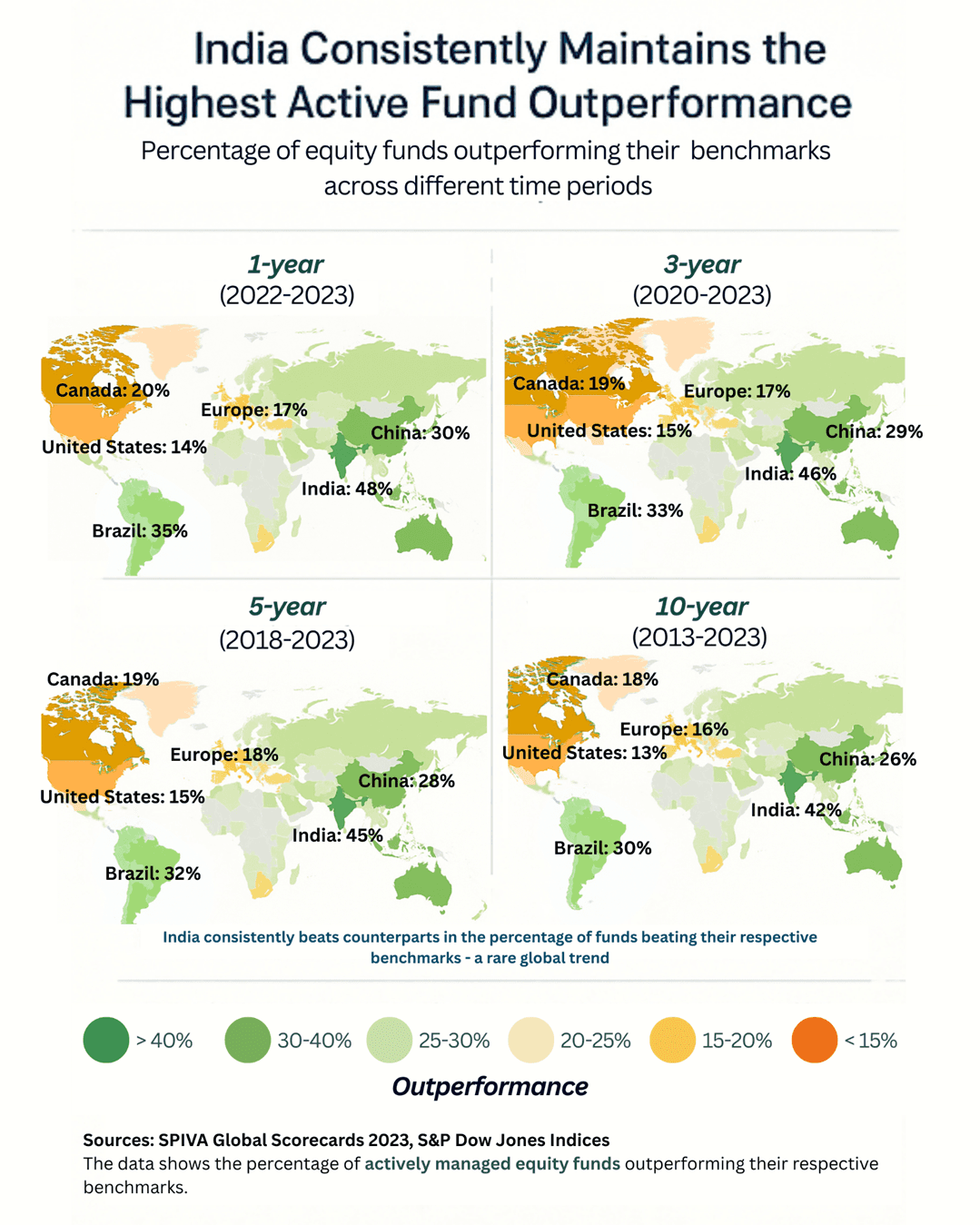

The numbers tell a sobering tale across developed markets. According to the S&P Indices Versus Active (SPIVA) Scorecard, an astonishing 92% of large-cap US active funds failed to outperform the S&P 500 over the 15-year period from 2007-2022. This underperformance isn't isolated to America—SPIVA's global data reveals systematic active management struggles with 85% of European equity funds, 79% of Japanese funds, and 83% of Australian funds underperforming their benchmarks over the same period.

The pattern becomes more pronounced over longer timeframes, with global outperformance rates declining from 38% (1-year) to just 15% (15-year) across developed markets. India stands as the remarkable exception, maintaining a 26% outperformance over 10 years—the highest globally by a significant margin.

This isn't merely a temporary blip—this divergence in performance represents a fundamental shift in developed market dynamics:

Market efficiency has peaked: With high-frequency trading dominating 50-70% of US equity volume and institutional ownership controlling 80% of market capitalization, pricing inefficiencies vanish within milliseconds.

Correlation Convergence: Individual stock movement has become increasingly synchronized in developed markets, with average pairwise correlation rising from 0.28 in 2000 to 0.48 in 2022, drastically reducing selection opportunities.

Investment Horizons Collapsing: Average holding periods have shrunk from 8.2 years (1960) to just 5.5 months (2023), prioritizing momentum over fundamental value.

The market's verdict appears clear: in highly developed markets, the cost of active management increasingly outweighs its benefits, driving the unstoppable rise of passive investing from 20% to 58% of US equity assets between 2014-2024.

India: Scalable, consistent Alpha

Cross the oceans to India, however, and a dramatically different picture emerges. 40-45% of Indian equity funds outperformed their benchmarks over the decade (2013-2023). The performance is even more impressive in the mid-cap segment, where research coverage and inefficiencies multiply—with 55-60% of active funds beating their indices over the 10-year period, delivering an average annual alpha of 2-3%.

This stark outperformance stems from structural market characteristics:

Persistent Inefficiencies: The average Indian mid-cap stock has only 3-4 analyst followers versus 15-20 for US equivalents, creating substantial information gaps.

Economic Velocity: India's 6.5-7.5% growth rate (compared to 1.5-2.5% in developed markets) creates continuous disruption and opportunity.

Retail Investor Surge: Demat accounts skyrocketed from 36 million in 2019 to over 110 million in 2023, introducing new market behaviors that sophisticated investors can capitalize on.

Lower Market Concentration: Top 10 stocks represent only 30% of Nifty 50, compared to 35% for the S&P 500, creating a broader opportunity set for stock selection and reducing index dominance.

Sector Diversity: Unlike the technology concentration seen in US markets, India offers balanced exposure across financials, consumer goods, and industrials.

India's Decade: The Double Alpha Advantage

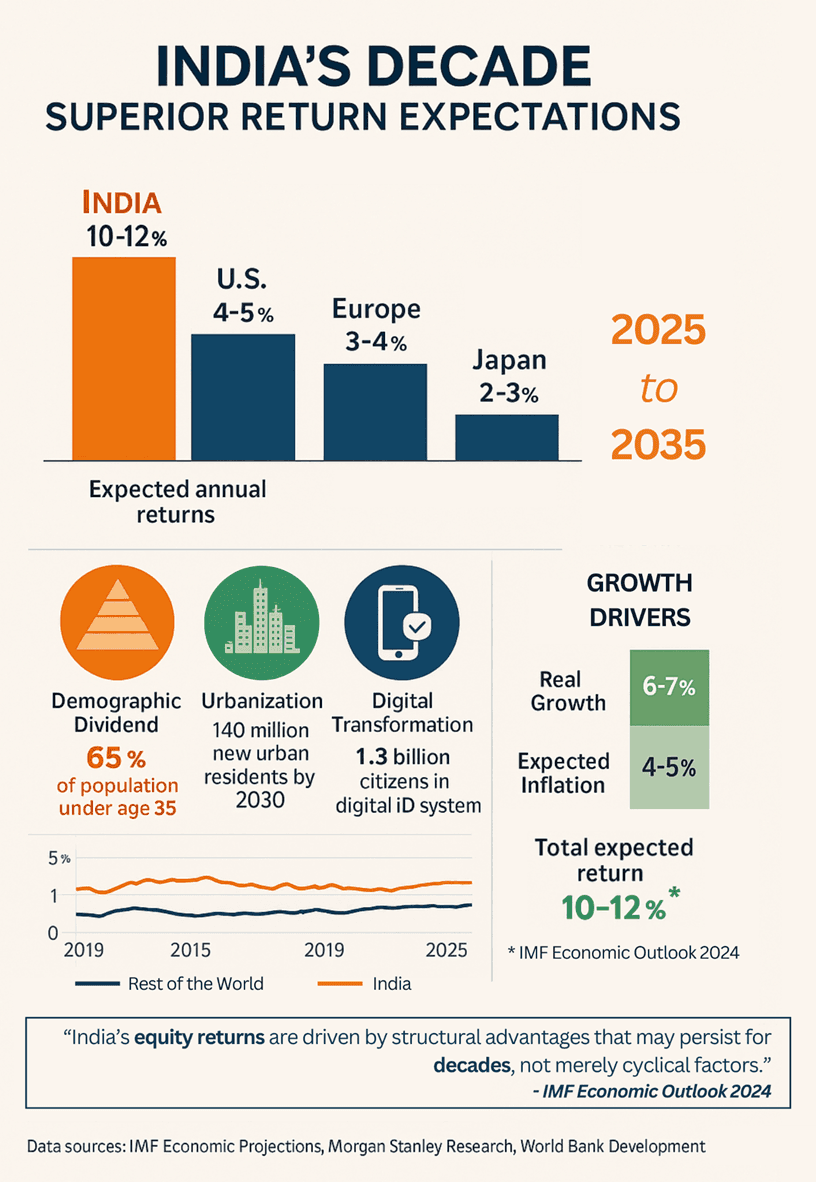

According to recent International Monetary Fund (IMF) projections, India's equity markets are poised to deliver exceptional returns of 10-12% annually over the next decade. This forecast derives from India's robust economic fundamentals: 6-7% real GDP growth, combined with 4-5% inflation, plus an equity risk premium of approximately 1-2%. These returns significantly outpace developed market expectations of 4-6% during the same period.

Even more compelling for sophisticated investors: when this superior baseline return is combined with the demonstrated alpha generation capabilities of India's active managers (2.5-3.2% annually over benchmark), the total expected return potential rises to 12.5-15.2%. This represents potentially double the returns available in developed markets even before currency appreciation factors.

This superior return outlook isn't merely cyclical—it represents India's structural growth advantages: a demographic dividend with 65% of the population under age 35, accelerating urbanization adding 140 million city-dwellers by 2030, and digital transformation that has created the world's largest biometric identification system connecting 1.3 billion citizens to the financial ecosystem. Unlike developed markets where active management is increasingly fighting a losing battle against efficiency, projections suggest India's inefficiencies will persist for at least another decade as institutional development struggles to keep pace with explosive market growth.

The Strategic Imperative: Maximizing India's Alpha Opportunity

India's distinctive market characteristics demand a specialized approach—one that fully leverages the persistent inefficiencies and structural growth advantages unique to this dynamic economy:

For Indian Market Exposure:

Prioritize skilled active managers with demonstrated expertise across India's diverse sectors and market caps

Focus particularly on mid and small-cap segments where inefficiencies are most pronounced and alpha generation potential reaches 3-4% annually

Seek managers with robust on-the-ground research capabilities who can identify emerging winners before institutional coverage increases

Capitalize on the information asymmetry provided by local presence and native understanding of India's complex business ecosystem

Consider the rapidly evolving Environmental, Social, and Governance (ESG) space, where 70% of India's ESG-focused funds outperformed in 2022, driven by governance improvements and sustainable growth initiatives

Develop strategic exposure to sectors benefiting from India's structural shifts: financial inclusion, infrastructure development, manufacturing expansion, and consumer premiumization

This approach enables global investors to fully capture India's dual advantage: superior baseline returns driven by macroeconomic fundamentals, enhanced by the alpha generation potential that remains elusive in more developed markets. With proper execution, this strategy positions portfolios to benefit from what may be the most significant wealth creation opportunity of the next decade.

Beyond Returns: Strategic Diversification

India's relative independence from global market movements offers genuine diversification benefits beyond alpha potential. During periods of global market stress when traditional correlations often increase, exposure to India's domestic growth story can provide valuable portfolio resilience.

Moreover, India's structural growth trajectory—powered by demographics, urbanization, and digital transformation—represents a secular opportunity that may span decades, complementing the more mature growth profiles of developed economies.

The Implementation Challenge

Despite these compelling advantages, implementing an India-focused active strategy presents significant hurdles for international investors. Navigating regulatory requirements, understanding local market dynamics, conducting proper due diligence, and managing currency exposures requires specialized expertise and infrastructure.

This is precisely where TresoWealth delivers exceptional value. Our platform provides seamless access to India's elite Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs), handpicked based on rigorous quantitative and qualitative analysis. We bridge the complexity gap, enabling global investors to capture India's alpha opportunity without the operational friction.

As markets evolve and efficiency patterns shift across geographies, those who recognize and act upon these structural differences position themselves at a significant advantage. Through TresoWealth, the path to India's alpha opportunity has never been more accessible—allowing investors to place their active management dollars precisely where they can work hardest.

In the geography of investment returns, knowing where to look for alpha may be the most important investment decision of all.

Sources:

S&P Dow Jones Indices. (2023). SPIVA® Scorecard

S&P Global. (2024). SPIVA India Scorecard - Year-End 2024

International Monetary Fund. (2024). World Economic Outlook

National Stock Exchange of India. (2024). NSE India Market Report

National Payments Corporation of India. (2024). UPI Product Statistics

McKinsey Global Institute. (2023). Digital India: Technology to Transform a Connected Nation

Morgan Stanley Research. (2023). India Economics: Digital Public Infrastructure